Click here to see all of my past Savings Reports and view my interactive net worth chart

Go to How To Track Your Savings to check out the Saving Ninja Super Spreadsheet.

Wow, what is going on with the world right now?

Trump is everywhere on my feeds and everything he’s doing seems super dystopian, but I’m unsure if this is as bad as it seems or it’s just my own social media algorithm, you never know these days - especially as I haven’t watched live TV for years.

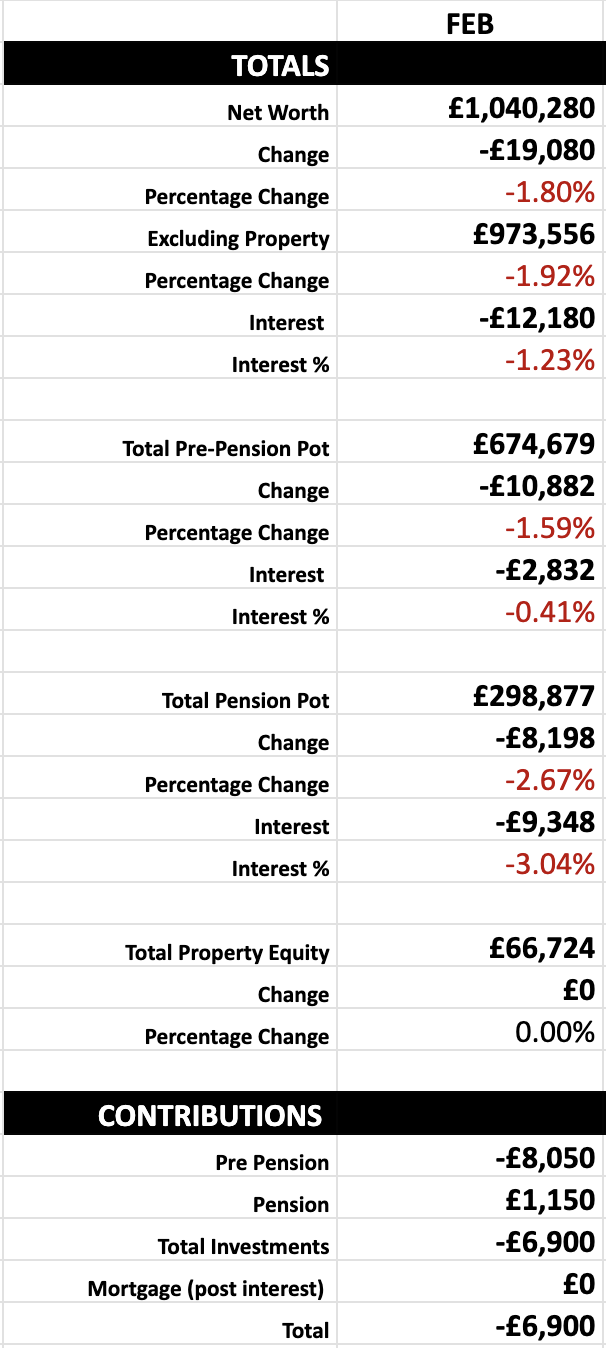

The stock market is down, but we’re still over a mil. This month, I realized that I’d calculated our capital gains tax incorrectly when I attempted to utilize the £3k gain earlier in the year.

In most places you can buy and sell stock as different units, they each have their own buy price. That’s why most platforms allow you to optimize tax by changing the sell settings to FIFO (first in, first out) or FILO (first in, last out). But, the UK, being their awkward selves requires you to calculate the average of all of that stock and have that as your buy price, this is called section 104 holdings. There’s also some complicated as hell maths for if you buy the stock again within 30 days (annoying if you’re still getting monthly RSU’s like I am,) it gets even worse to calculate when you’ve sent some stock to your spouse like I have.

So, what I thought was a perfectly calculated £3000 capital gain was actually a £450 loss due to getting RSU’s within 30 days worth less. So, after days figuring it all out using a lot of spreadsheets and online calculators, I’ve sold another £8000 worth of stock. Hopefully, I’ve done it correctly this time and both me and Mrs SavingNinja have used up our £3000 capital gains allowances before the end of the tax year (unless my company stock drops again!) Stupid rules.

Cash Is Growing

We’re sitting on around £35k of cash right now. I’m still hoping we can get as close to £156k as we can before September so we can pay off our mortgage while we sell the property instead of moving to a retail price interest rate (around 7.7% last time I looked.)

I’m still planning on stoozing 0% interest credit cards to help us get there, but I’ve currently only got a single card with a £3500 limit (Barclays,) I’m hoping to find more!

I’ll make up any shortfall with a margin loan on IBKR as this will still be much cheaper than the retail mortgage rate. I think this should be relatively safe to do if borrowing £50-100k as the general investment account currently sits at around £500k, so 10-20% margin. I need to read up more about this closer to the time, though. Anyone got any advice?

House

On the topic of our old house. We’ve decided to move back into it. The tenant has moved out and we’re currently renting. We’re also not liking our current rental and are struggling to be accepted onto any others (with a cat and a baby.) That coupled with the worry of the house sale taking a long time, possibly even longer than a year, it made financial sense to move back in. It’s going to roughly save us £1300 per month in rent and council tax.

Last month we went on a trip to the house to see if it would be viable with a baby. While it’s not perfect, it’s manageable, but we probably wouldn’t want to stay there for longer than a year. It’s good in a way as it forces us to make plans for our future and where we want to settle long-term as we know that we’ll have to move again.