Click here to see all of my past Savings Reports and view my interactive net worth chart

Go to How To Track Your Savings to check out the Saving Ninja Super Spreadsheet.

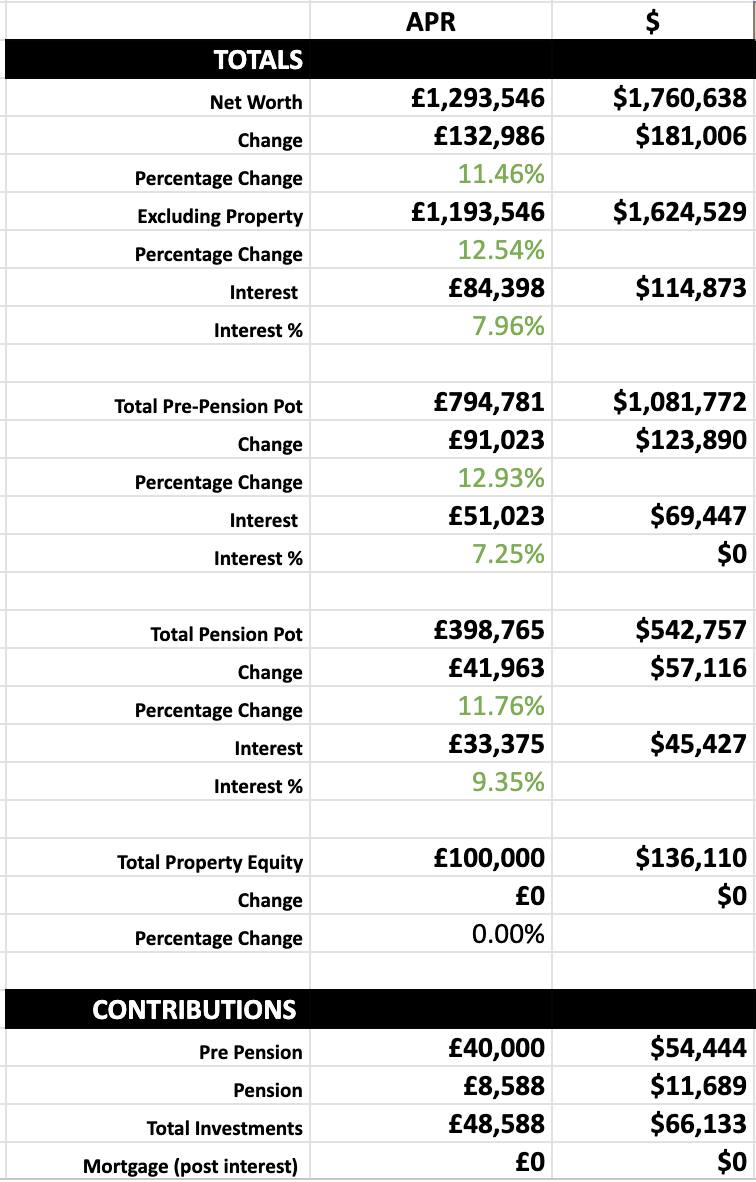

This month saw the markets recover, and it coincided with investing £40k into our ISA’s so we saw a big bump in net worth. We crossed the $1m invested outside of our pensions, £900k in GBP, close to £1m! And our total net worth went up to £1.3m.

We explored Scotland for the first time this month and had an amazing time! The Cairngorms is beautiful and a lot of the hikes we went on reminded us of where we lived in New England.

Scotland is looking more and more like the place we’ll end up moving to. We have to decide when, though, as with my current salary we will lose over £1k per month with the increased Scottish tax burden, so staying outside of Scotland while I continue to work and moving when I no longer have my high salary may be better, this would mean putting off our house purchase though (and potentially house prices rising?)

We’ve began to look at houses anyway to see what’s out there. I’ve been fretting a lot this month over how much to put into a house purchase and house much of a mortgage to get.

Traditionally, the advice is to keep invested in the market as a mortgage is one of the best loans that you can get. But with mortgages costing 4.5% and when the alternative is a general investment account which owes 24% on gains, the proposition looks a lot less appealing.

We would need to earn 6-7% in the general investment account to keep up with the cost of the mortgage, so if we bought in cash, it would be a risk free 6-7%. When the market is high and we don’t have to deal with sequence of return risk for this investment, it seems like the best bet.

Psychologically, for me, it would be very difficult to take £500k out of our pre-pension savings (and pay £40k in capital gains tax) and put it into a house as right now that would only leave £400k invested which would have to last us 25 years until we can access our SIPP’s. That doesn’t seem very plausible, but it is seemingly a less risky bet than having £800k invested and taking out a £400k mortgage at 4.5%.

If the market crashed, a mortgage would be the only path forward while it recovered.

I’m going to re-evaluate in a year when we are going to seriously consider buying. Hopefully our investments continue to do well and the decision won’t look as daunting.

I’m gutted that we don’t have a 1.2% interest rate environment anymore, it would make this decision much simpler, where the obvious default would be to just get the biggest mortgage possible and leave everything else in the stock market.

Of course, another option would be to find a cheaper house, but the type of property we want, with the space to potentially house 2 kids while both parents work from home, it seems £500k is the floor, even in rural Scotland. And it’s kind of frustrating that our total net worth would support this, but if I don’t want to keep working, we can’t count the SIPP until much later.

Mortgage rates being lower would make it so much easier! My generation have really got screwed over the most, eh?

Anyway, that’s it for this month. We’ll be going to Scotland again in May and I’ll be going on a work trip.

Have a good month!